Business

Meet Ajayi Joshua Oluwatobi: The Visionary Founder Of Nord Automobile Limited

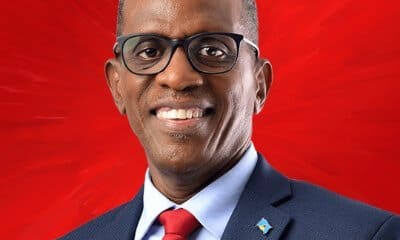

Ajayi Joshua Oluwatobi is a 36-year-old trailblazer revolutionizing the automotive industry with his innovative spirit and relentless drive. Born in 1988, he attended Nigeria Navy School and later studied Soil Sciences and Farm Mechanization at Olabisi Onabanjo University. He recently completed his MBA at Lagos Business School, Pan-Atlantic University, Nigeria.

Ajayi’s career took off in 2012 at Mercedes-Benz Nigeria, where he managed the van division and grew market share from less than 1% to 7% between 2013 and 2015. He won the Mercedes-Benz Best Sales Performance award for Africa in 2013. Visits to Mercedes-Benz factories in Europe and Asia inspired him to build a Nigerian global auto brand.

Read also : Diaspora Diva: Meet 21 year Catherine Mbagwu, Maryland-born

In 2015, Ajayi co-founded Jetvan Automobiles Limited, serving as CEO until 2018. He then left to focus on building Nord Automobile Limited, assembling elegant, reliable, durable, and cost-efficient vehicles. Today, Nord Automobile is valued at over N4.2 billion.

Ajayi’s values include visionary leadership, innovative spirit, perseverance, excellence, and Nigerian pride. He’s a true pioneer in the automotive industry, pushing boundaries and redefining what’s possible.

Rubio vows US will keep protecting Gulf shipping, says diplomacy with Iran still possible

By Boniface Ihiasota, Washington DC

United States Secretary of State, Marco Rubio on Wednesday said Washington would continue military operations to safeguard international shipping routes from Iranian attacks while insisting that the U.S. remained open to a diplomatic resolution of the crisis.

Rubio, who spoke to journalists in Manila, accused Iran of undermining previous commitments by continuing attacks on commercial vessels transiting a key international waterway.

He said Tehran had failed to uphold an earlier understanding that called for unrestricted maritime navigation, arguing that the latest attacks demonstrated Iran was “not serious” about diplomacy.

“We remain open to diplomacy. We remain open to working it out in a negotiated way. But right now, they don’t seem to be serious about that,” Rubio said.

According to him, the U.S. military would continue targeting sites allegedly used to launch attacks against commercial shipping while protecting vessels passing through the strategic maritime corridor.

“Ships are trying to go through the straits, and they’re getting blown up. The United States is defending that shipping and degrading Iran’s ability to target global shipping,” he said.

Rubio also rejected suggestions that Washington’s objective was to force Iran into submission, arguing instead that the U.S. was determined to prevent Tehran from acquiring nuclear weapons.

He claimed Iran had spent decades investing heavily in missiles, drones and proxy groups instead of addressing domestic economic challenges, including soaring inflation and rising food prices.

The U.S. Secretary of State urged more countries to join efforts to secure international shipping lanes, saying many nations depended more heavily on the affected maritime route than the United States.

Although Washington had not made fresh requests during meetings with Asian allies in Manila, Rubio disclosed that previous discussions had explored possible contributions, including naval mine-clearing capabilities.

He maintained that the U.S. would prefer a negotiated settlement but insisted that freedom of navigation could not be compromised.

Rubio also confirmed he would meet Russian Foreign Minister Sergey Lavrov to discuss the war in Ukraine, saying Washington remained willing to play a constructive role in efforts to end the conflict while pursuing cooperation with Moscow on other strategic issues.

Marketers Import Dangote-Refined Fuel Through Togo Hub

Nigerian fuel marketers are increasingly importing refined petroleum products produced by the Dangote Petroleum Refinery through an offshore trading hub in Lomé, Togo, in a development that underscores the refinery’s growing influence on fuel supply across West Africa.

The disclosure was made by Matthew Tracey-Cook of S&P Global during a webinar organised by the Major Energies Marketers Association of Nigeria.

The webinar, themed “West Africa Pricing and Flows in the Context of the War,” examined evolving fuel supply chains and pricing trends within the region.

Speaking during the session, Tracey-Cook said refined products from the Dangote Refinery are being exported on a coastal basis to Lomé before being re-imported into Nigeria by fuel marketers.

According to him, the trend reflects the increasingly interconnected relationship between the Lagos-based refinery and the offshore ship-to-ship trading hub in Togo.

He noted that despite Dangote’s growing capacity to supply the domestic market directly, some marketers continue to source products through Lomé, a development that may be linked to pricing differences between local and international markets.

Tracey-Cook, however, stressed that the Togolese hub remains a strategic logistics centre for fuel distribution across West Africa.

According to him, the facility continues to handle significant fuel volumes and remains slightly larger than it was in 2024.

He added that volumes transacted through Lomé surged in certain periods, particularly in November and December 2025, surpassing volumes recorded on several other regional supply routes.

The S&P Global official explained that the hub plays a vital role in regional fuel distribution by receiving large medium-range tankers and transferring cargoes to smaller vessels capable of accessing ports with limited infrastructure.

Ghana eyes local takeover of Gold Fields’ Tarkwa mine

Ghana may transfer control of the Tarkwa gold mine, currently operated by Gold Fields, to local mining firms when the mine’s leases expire in April 2027, as the West African nation seeks to deepen local participation in its lucrative gold industry and maximise benefits from rising global gold prices.

According to a Bloomberg report, Ghanaian authorities are considering inviting local companies to bid for the operation of the Tarkwa mine, although discussions remain at a preliminary stage.

The government is also weighing the option of renewing the leases held by Gold Fields.

The move forms part of Ghana’s broader strategy to increase its share of mining revenues and strengthen indigenous ownership within the sector.

The country, Africa’s largest gold producer, has in recent years introduced measures aimed at boosting state earnings from mining activities, including increasing gold royalties from five per cent to as much as 12 per cent.

Should the government proceed with the plan, interested Ghanaian firms would be required to submit bids for evaluation.

Officials are expected to assess proposals based on commitments to environmental restoration, job creation, and infrastructure development in mining communities.

The potential loss of the Tarkwa mine would represent a significant setback for Gold Fields, as the operation contributed about 20 per cent of the company’s total gold production in 2025. The mine produced approximately 475,000 ounces of gold during the year.

Responding to the development, Gold Fields said it had already submitted an application for the renewal of the Tarkwa mining leases and remains engaged with the Ghanaian government.

“We have submitted an early application for the renewal of the Tarkwa mining leases. These constructive engagements are continuing,” the company stated.

Authorities believe local ownership of the mine could create more opportunities for Ghanaian engineers, contractors, suppliers and entrepreneurs, while ensuring that a greater share of mining wealth remains within the country.

Gold Fields Chief Executive Officer, Michael Fraser, had earlier disclosed that the company was developing a 20-year operational and investment plan for the Tarkwa mine.

The latest development follows the transfer of Gold Fields’ other Ghanaian asset, the Damang mine, to the state after its lease expired earlier this year.

Following a competitive tender process, the mine was awarded to Engineers and Planners Co. Ltd., a Ghanaian firm with existing mining contracts at both Tarkwa and Damang.

EDITORIAL: Tackling Poverty in Africa

Spain battles political fallout as 60,000 migrants overwhelm Ceuta border

Hamas agrees to disarm as Gaza withdrawal deal gains momentum

Pastor Jerry Eze Defends Miracles At UK Conference Amidst Criticism And Controversy

Diaspora Watch 20th Edition (October 14-20, 2024): Your Trusted Source for Global News and Insights

Tanzanian Man Reportedly Dies And Returns To Life Six Times

-

Milestone3 days ago

Milestone3 days agoNigerian bags HVAC Engineering degree in US, lands full-time job

-

Analysis3 days ago

Analysis3 days agoLessons from the Catholic Bishops’ Visit to Tinubu, by Boniface Ihiasota

-

News3 days ago

News3 days agoCARICOM chair renews reparations demand

-

Analysis3 days ago

Analysis3 days agoObasanjo, Atiku and the Burden of Broken Trust, by Alabidun Shuaib AbdulRahman

-

News2 days ago

News2 days agoSpain battles political fallout as 60,000 migrants overwhelm Ceuta border

-

News2 days ago

News2 days agoHamas agrees to disarm as Gaza withdrawal deal gains momentum